Posted: May 29, 2020 | Adam Moskowitz

Does PACE work with HUD financing? Yes.

In fact, the potential for PACE financing to complement HUD Financing is a trending topic in the PACE industry covered by both the US Department of Energy's C-PACE working group and PACENation in recent virtual workshops.

Meeting development, sustainability and social goals:

Recent attention to the relationship between PACE and HUD makes sense, as lenders look to the strength and potential of the multifamily market and city governments look for economic development opportunities that sync with goals to provide affordable housing while meeting carbon reduction standards. Considered in the context of the COVID-19 shelter-in-place orders, which highlight the importance of safe, comfortable and affordable housing, the potential for the positive impact of an additional capital source such as PACE is even greater.

"Affordable housing is an important focus for every urban planning department," suggested CounterpointeSRE managing partner, Eric Alini who moderated the PACENation session on HUD financing. "PACE financing can help with some affordable housing issues including energy injustice by making capital available to this sector."

PACE is in the right places:

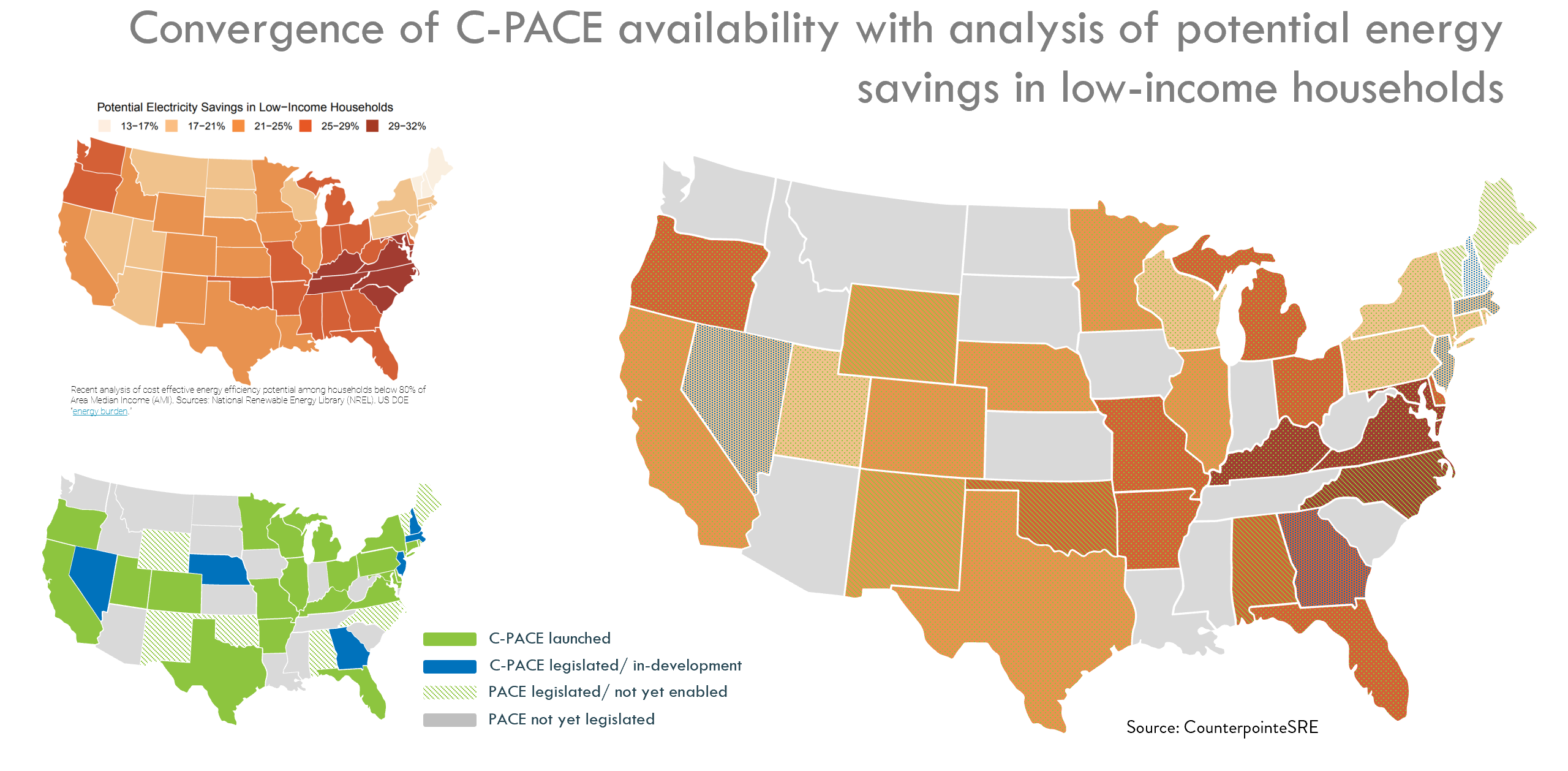

Alini pointed to data from the Department Energy and National Renewable Energy Library (map upper left) that suggests the highest possible return on investment for electricity savings in low-income families aligns closely with existing and emerging PACE programs (map bottom left). The resulting map at right below demonstrates the convergence of PACE availability and high potential for energy savings in low income households.

The myth is busted, but the path is narrow:

Since the issuance of guidelines of HUD guidelines in 2017 (linked here) there has been little PACE funding on HUD properties, resulting in the myth that HUD won't approve PACE. This was not the intention of the guidance, nor is it the posture of the agency based remarks by Bob Iber, Senior Advisor, Office of Multifamily Housing Programs for the U.S. Department of Housing and Urban Development.

"I will note that when we put together the pace housing notice 2017-01 we did work with PACE administrators in three states to make sure we were getting it right, but since we issued the notice in 2017 we've approved two deals and clearly that's a low number and we'd like to see if there is a way we could improve," stated Iber during the PACENation workshop entitled "Expanding Access to PACE for Multifamily Housing," held on May 28th.

Bob Iber and his colleague Rick Daugherty, Asset Management Branch Chief for the US Department of Housing and Urban Development detailed the basic premises of the guidance, but suggested flexibility and the ability to waive certain items when presented with an actual deal. For instance, the guidelines specify an opinion letter from the property's State Attorney General must accompany a loan package stating, "that the obligations are special assessments and treated in a similar matter as the real estate taxes."

This letter has proven difficult to attain in certain states, but has been received from a few jurisdictions with others a work in progress. The flexibility offered here was that while required, the opinion could come from the office, not necessarily the AG him or herself.

What remains required:

- Owner's compliance with basic HUD requirements

- savings to investment ratio of 1:1

- underwriting based on 75% of estimated energy savings

- adherence to HUD programmatic debt ratios

"It's important to note that when we wrote the guidance we thought we would mostly see PACE for existing properties with FHA insurance and or section 8 or we held the loan," recalled Iber.

The best opportunity according to HUD:

"A mature project, wanting to upgrade its energy efficiency using PACE only, without new financing other than PACE, is really the ideal project for a good fit and really was the focal point of the notice," suggested Rick Daugherty in the PACENation workshop.

Daugherty noted that most of the agency's FHA loans wind up in Ginnie Mae pools thus suggested the following for the target PACE-financed HUD property:

- the ideal property would be mature (to some extent)

- it would have existing financing that is going to stay in place

- the owner wants to use PACE to supplement that financing to support efficiency or renewable upgrades

- the assumption is that the mature property has increased in value and its rents have increased over time

"These factors together should help create the room, within the original loan parameters for debt service coverage and LTV for PACE to be comfortably added without increasing any risk to the Ginnie Mae investors or to HUD," stated Daugherty.

On background:

PACE (Property Assessed Clean Energy) financing is a form of commercial finance that allows for the private funding of energy saving capital improvements to new or existing properties through the property tax bill. The program is enabled in more than 20 states and several cities and is widely used for most commercial property types. Programs vary state by state, but with few exceptions for small loan amounts, primary lender consent is needed for a special assessment (the PACE financing) to be attached to the property. Herein lies the critical relationship with HUD, which is of course the U.S. Department of Housing and Urban Development through which most affordable housing is financed.

Next steps:

Should you have a project that appears right for PACE financing, please inquire by clicking "get a quote," above.

Thank you's:

PACENation for hosting the virtual workshop from which the conversations with HUD representatives were extracted and to Kimberly Lewis, SVP of market transformation at USGPC, who led an initial panel on the subject of HUD and PACE at a prior PACENation event.